Predictive Reserving Analytics

Go Beyond Traditional Actuarial Models

Model calendar period effects and produce a full predictive distribution.

Model calendar period effects and produce a full predictive distribution.

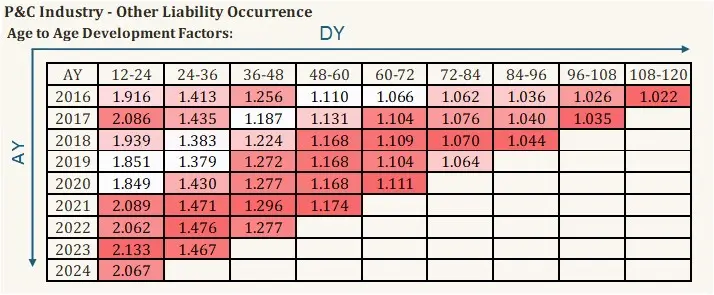

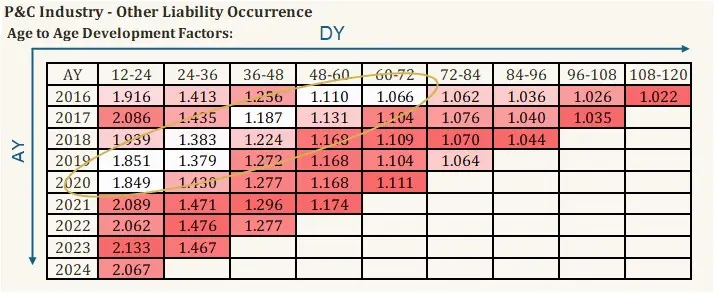

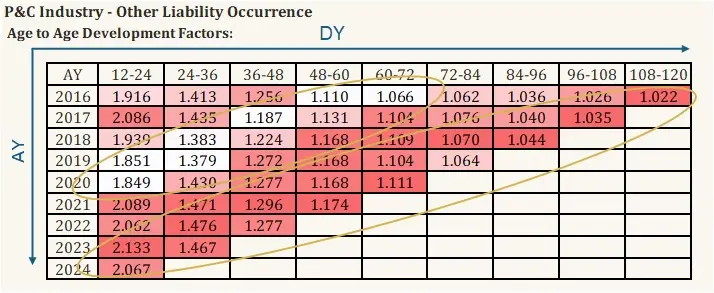

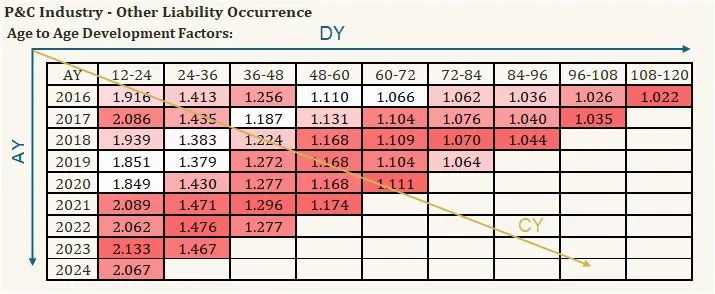

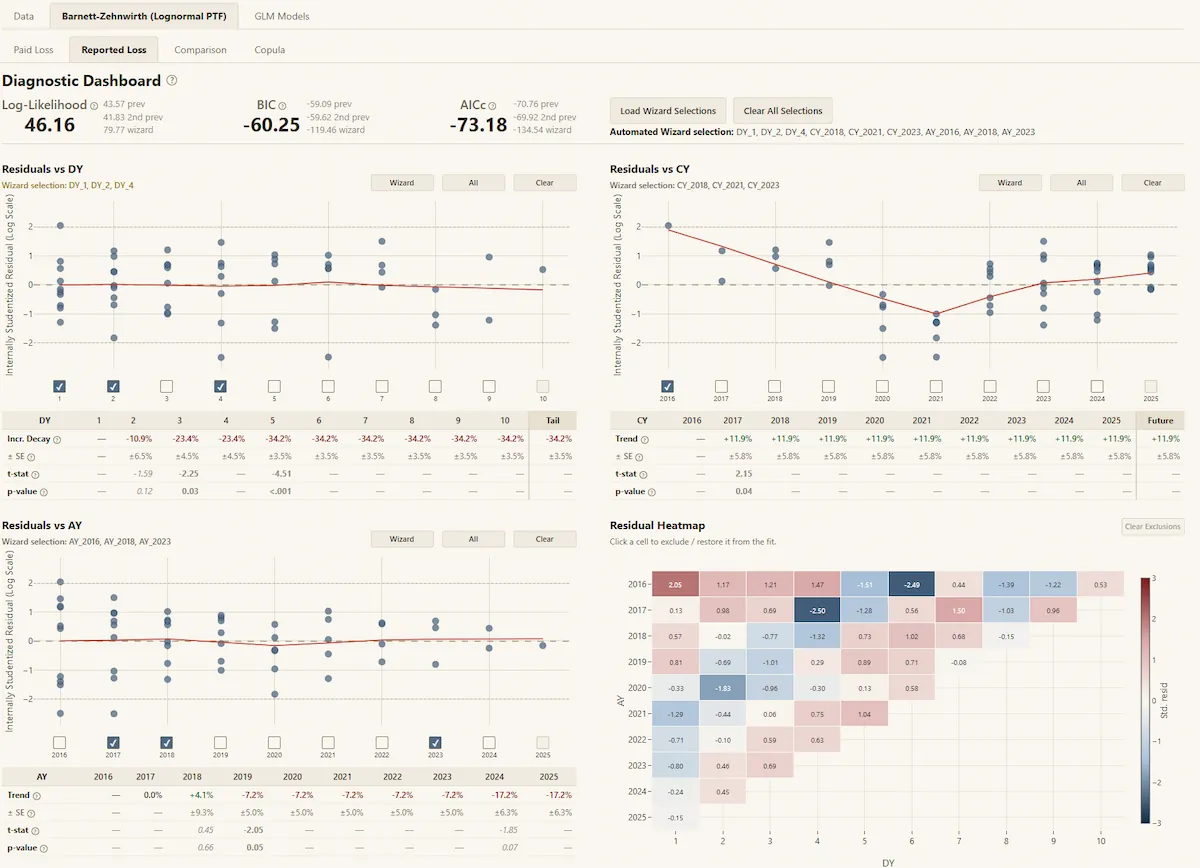

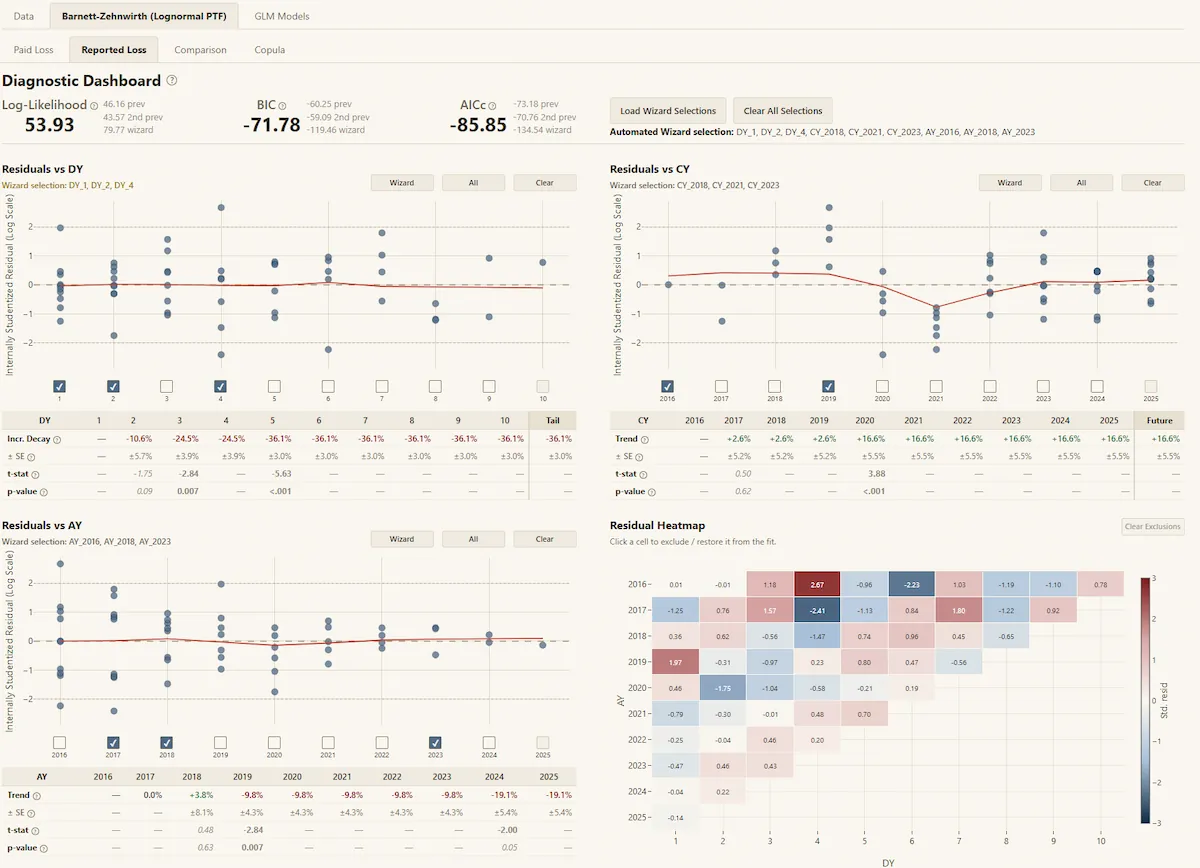

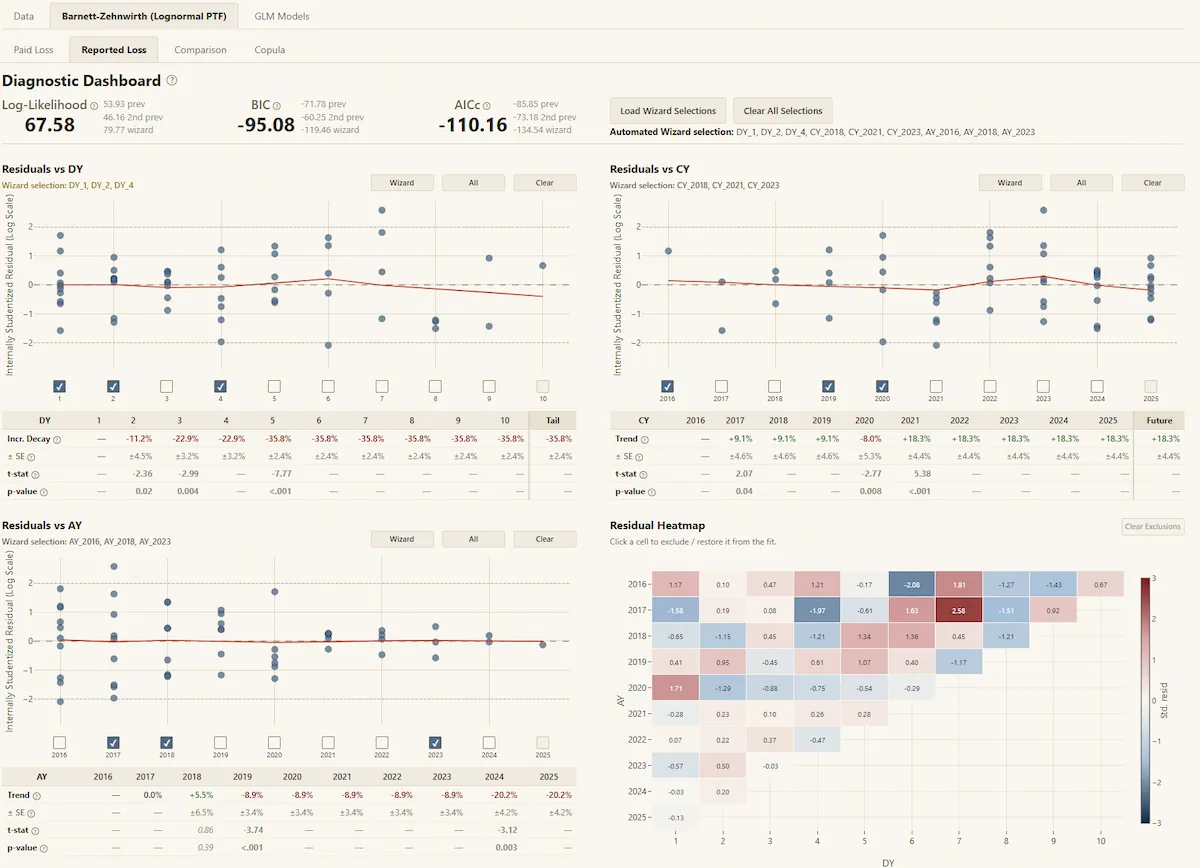

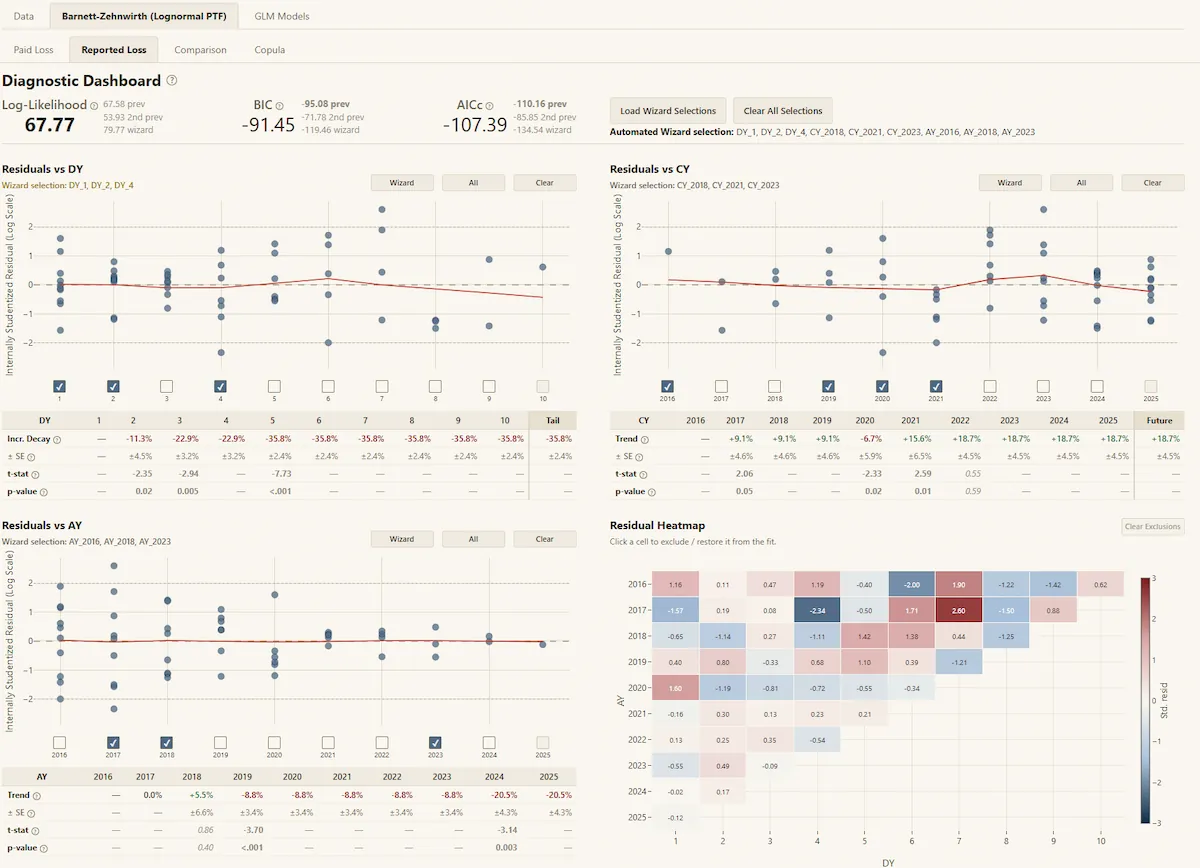

BASR is a modern stochastic actuarial software application providing a customizable statistical framework to properly model loss development triangles in three dimensions: accident period, development period, and calendar period.

Traditional deterministic actuarial reserving methods model losses in only the accident and development period dimensions, implicitly assuming calendar period effects are immaterial. With the pandemic skewing (at least) two calendar period diagonals and social inflation running rampant in many P&C lines of business, many of the traditional model assumptions are violated, and it is now more critical than ever to properly model and control for calendar period trends in the estimates directly.

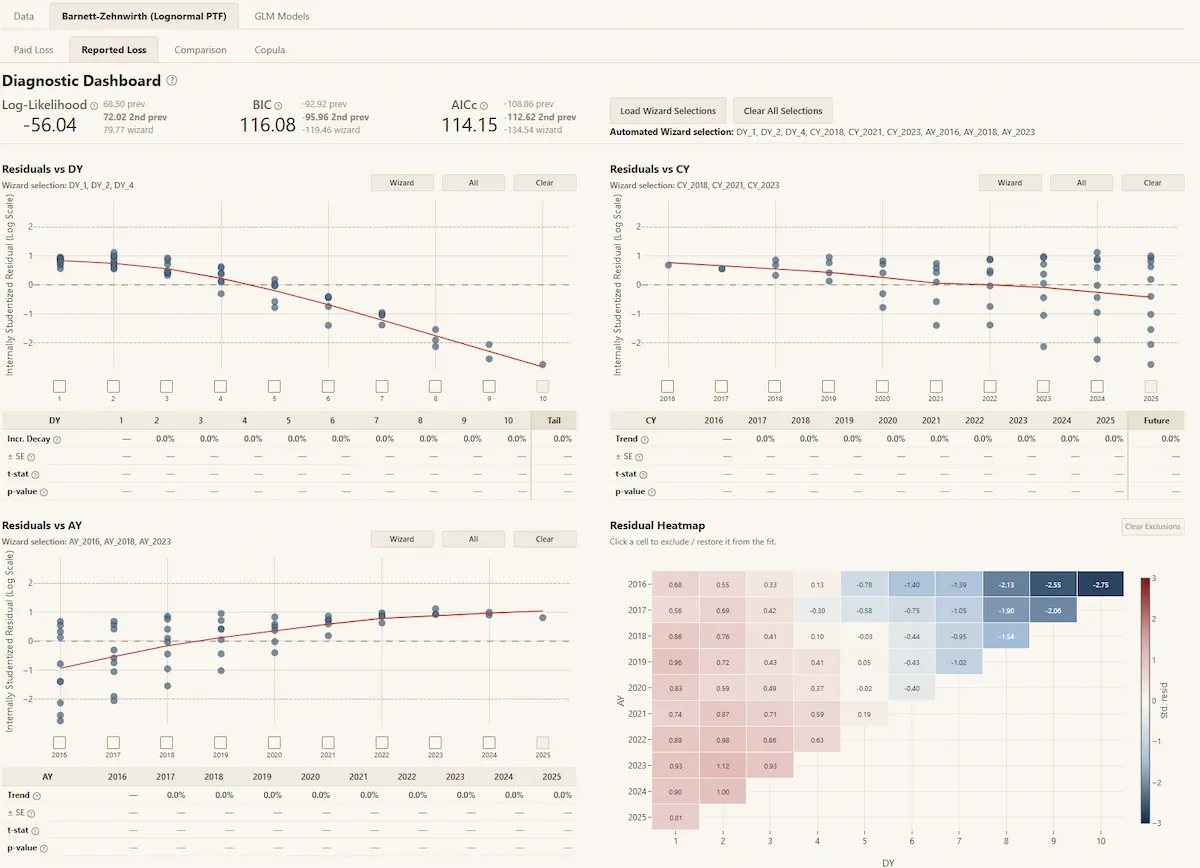

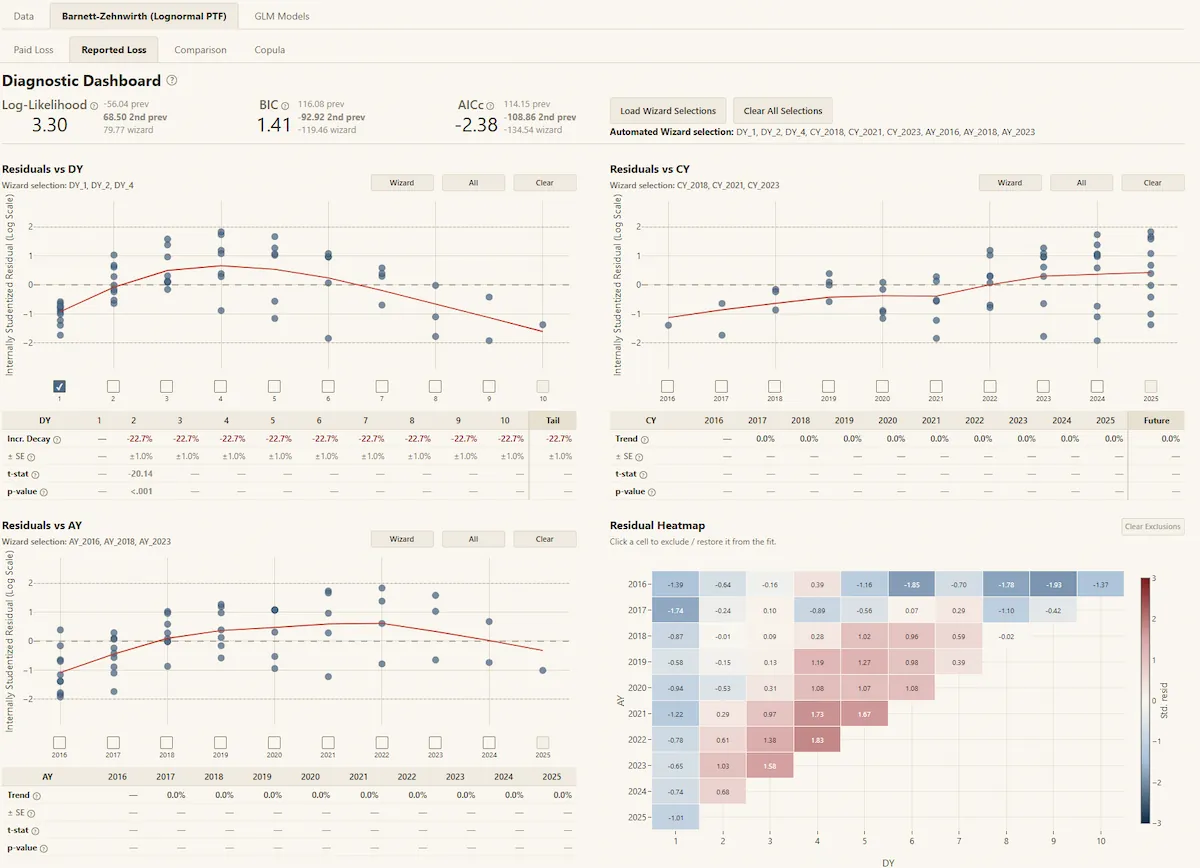

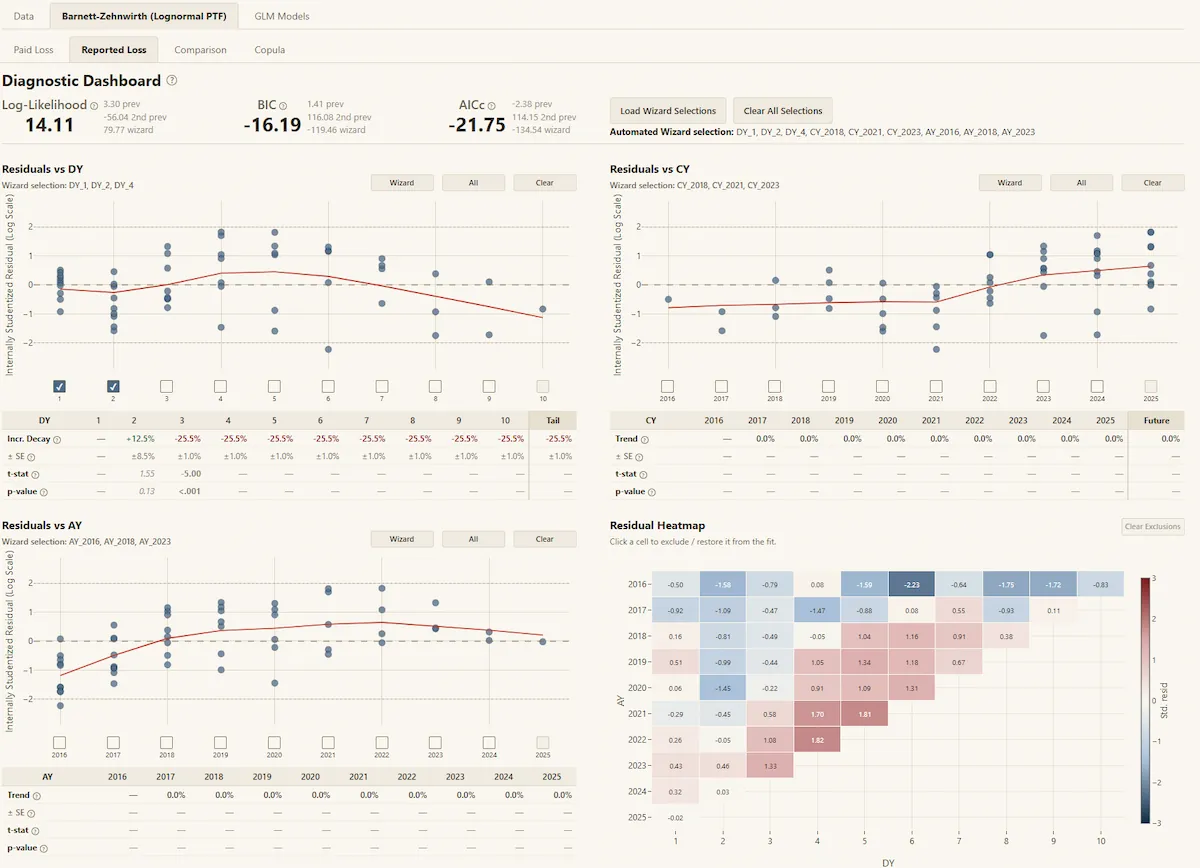

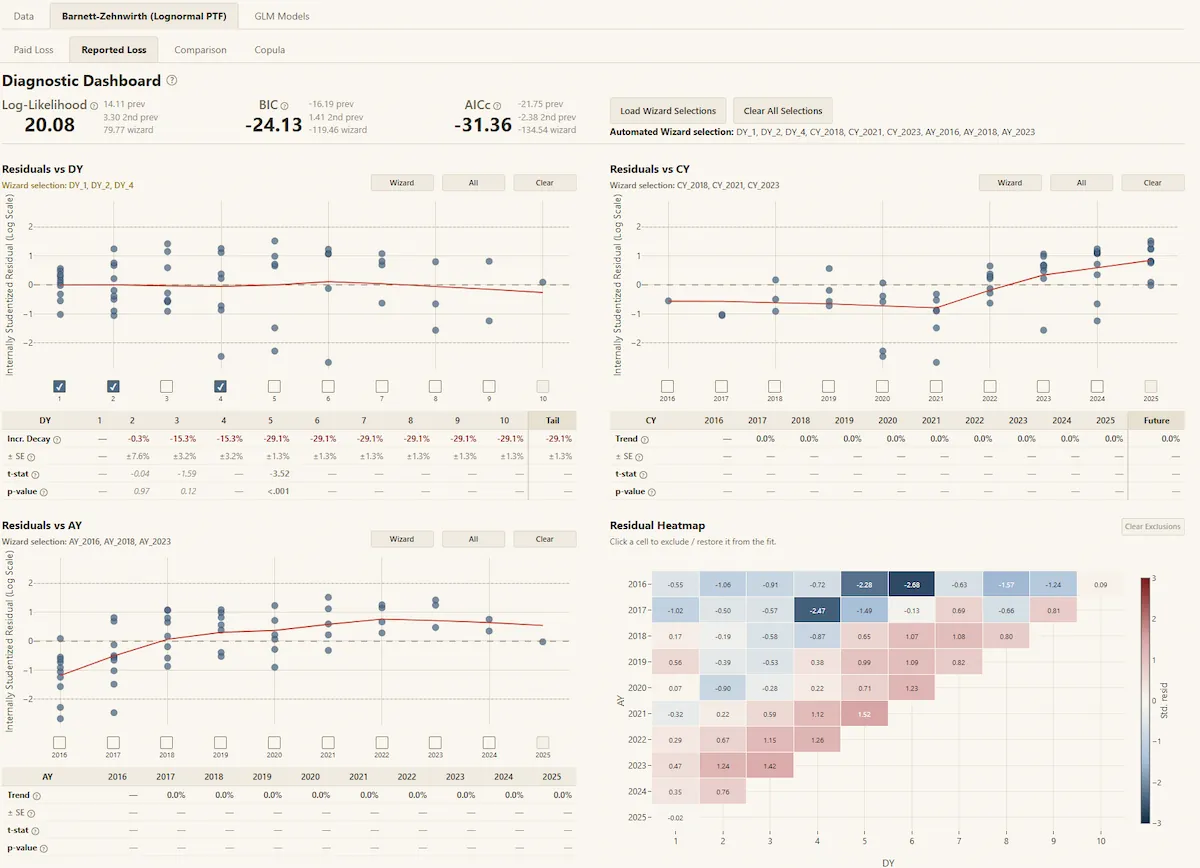

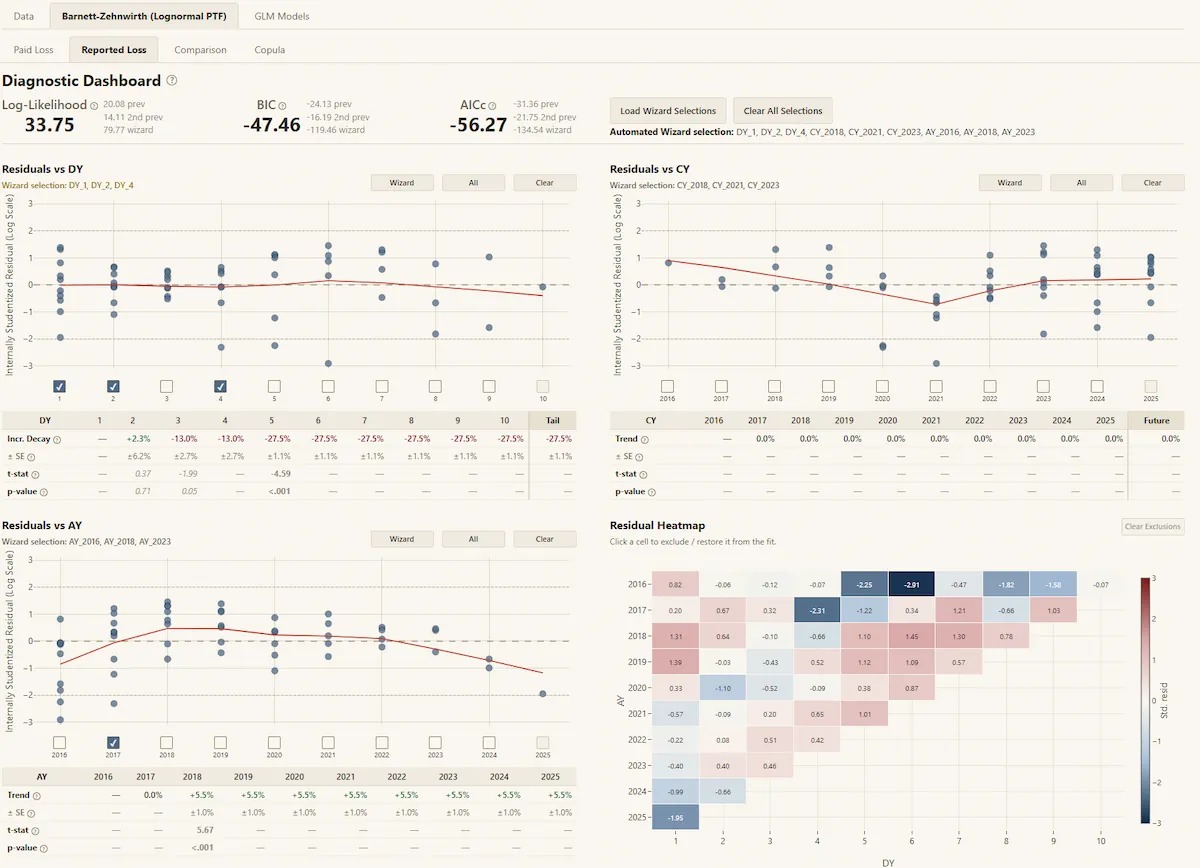

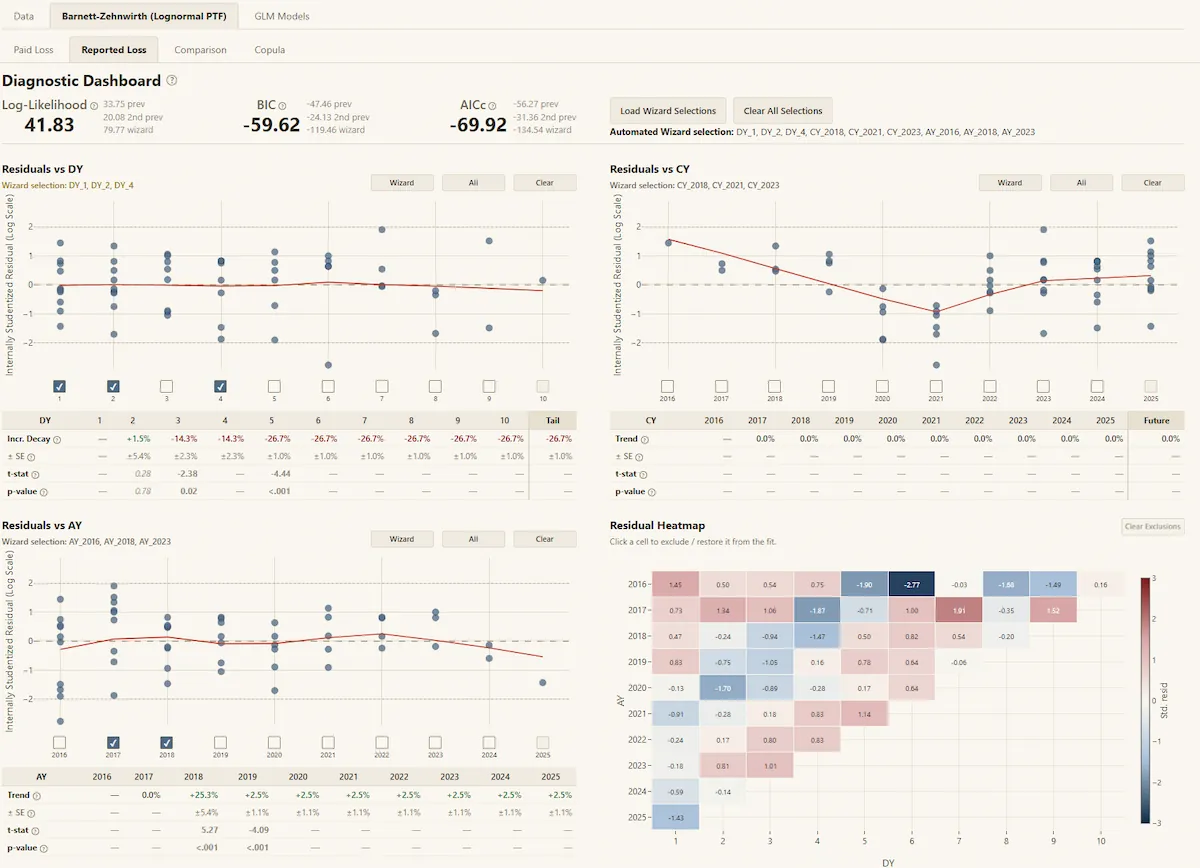

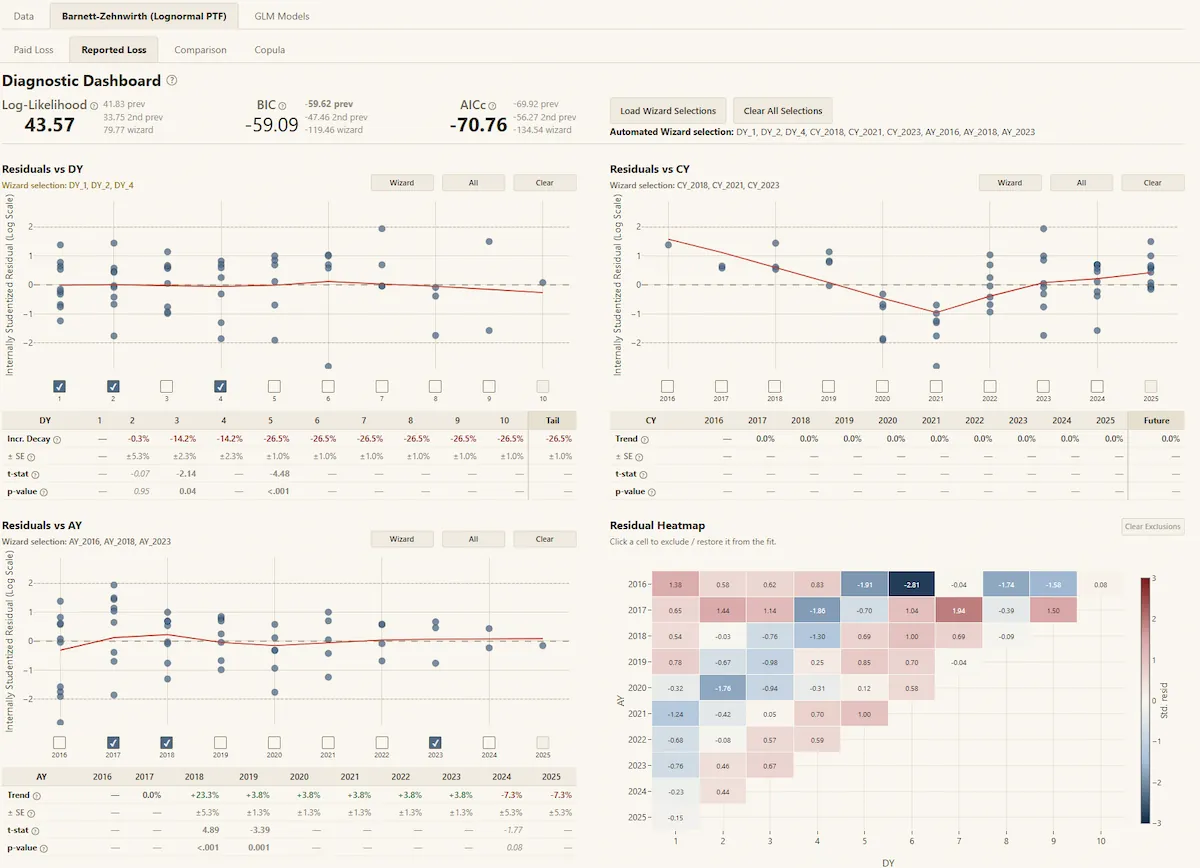

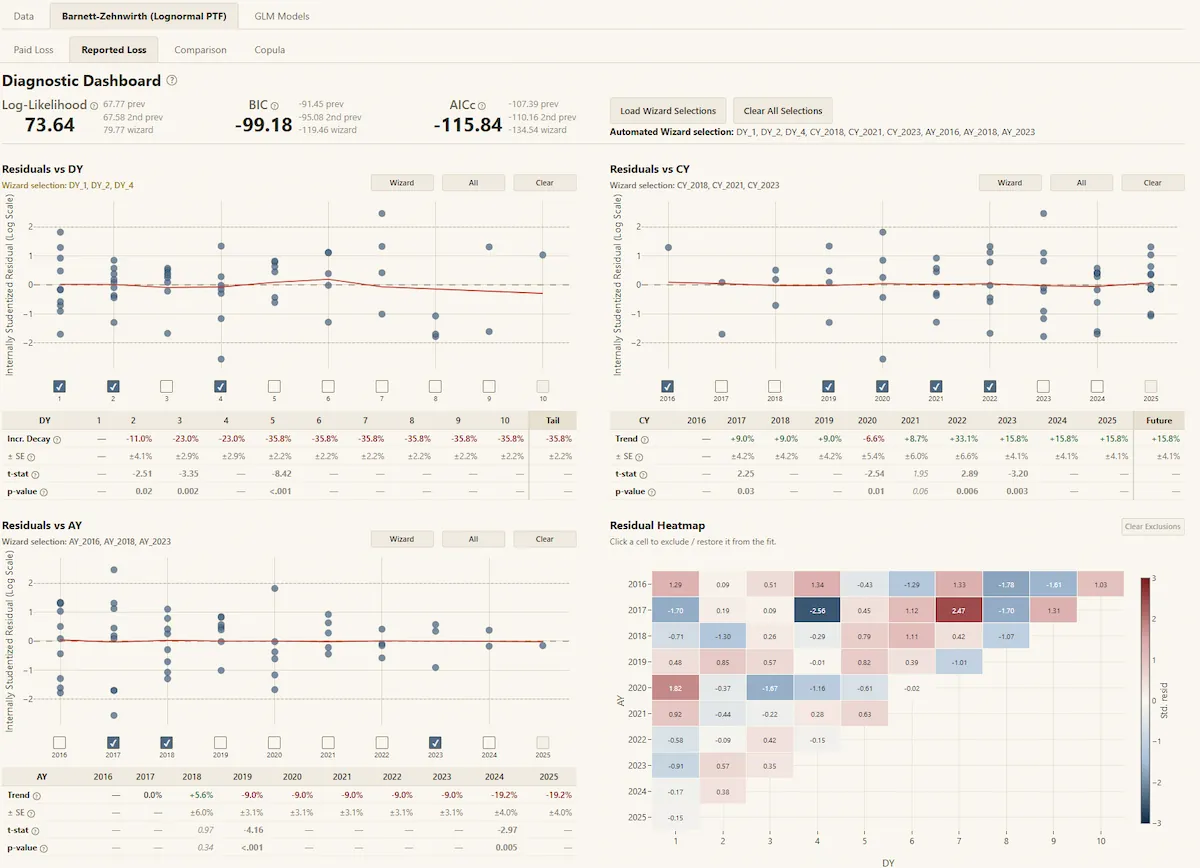

BASR's probabilistic modeling framework separates the trend structure (the signal) from random variation about it (the noise) and quantifies both process and parameter uncertainty in the projections. Statistical diagnostics of the model fit in all three directions (and overall) let the actuary quantify reserve uncertainty and form a narrative around observed trends, selections, and early warnings, not just provide a single number.

BASR includes an automated wizard that selects parameters based on the criterion of your choice (BIC, AICc, or likelihood ratio testing), giving a statistically principled reference point that can be refined by the actuary to incorporate knowledge of the underlying business and exposures.

The customizable model structure allows the user to select from various model forms, including the Barnett-Zehnwirth Probabilistic Trend Family (PTF) modeling framework, widely considered the gold standard of stochastic reserving methods and described in their paper “Best Estimates for Reserves” (published in the Proceedings of the CAS, Volume LXXXVII, 2000), and the GLM family distributions: ODP, Gamma, Inverse Gaussian, and Tweedie.

Each model links the variance to the mean, but the GLM families fix that relationship across the entire triangle, while the PTF framework allows it to change across development periods (e.g., higher percentage variability is often appropriate for later development periods, which remain noisy even as the incremental mean becomes small), which is often a material enhancement.

All of these structures provide clear advantages over the standard two-dimensional ODP Bootstrap (simplified GLM) in both insight and control.

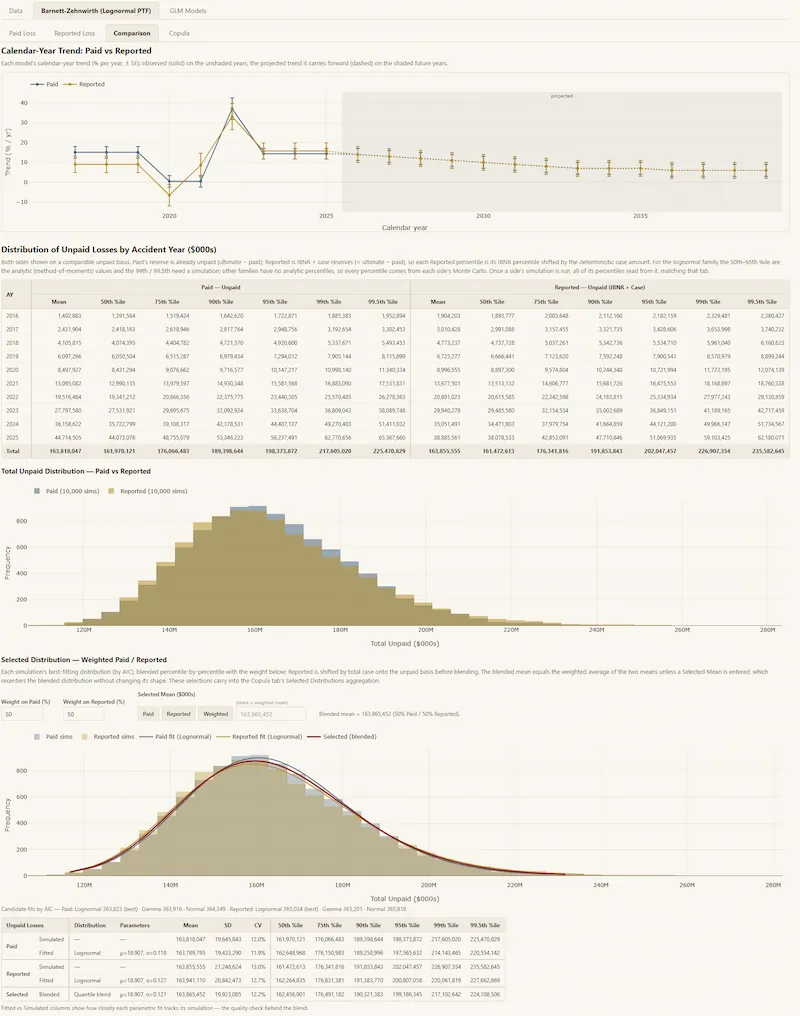

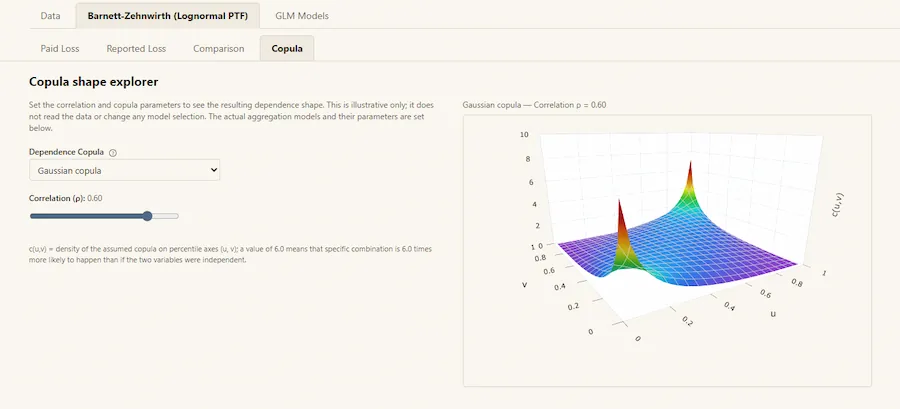

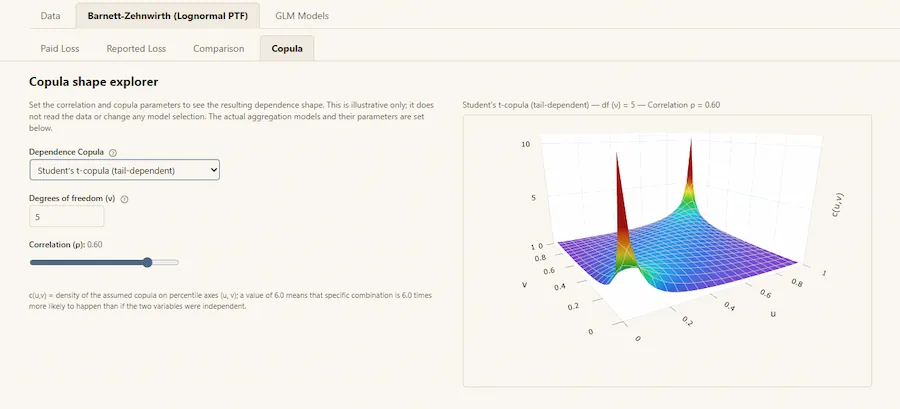

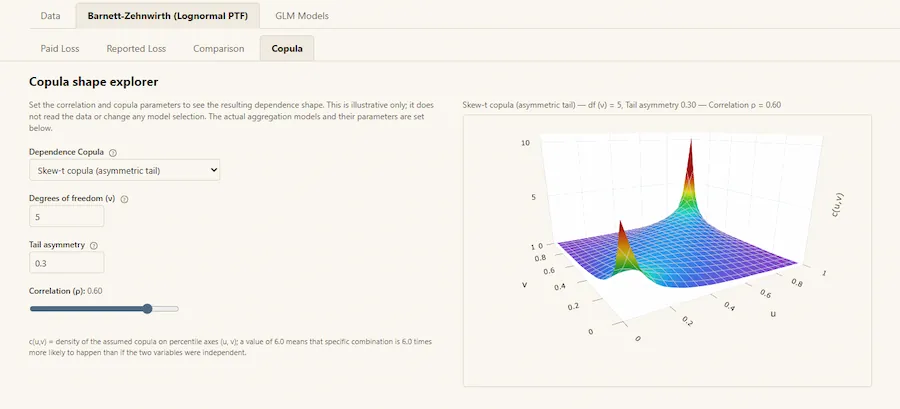

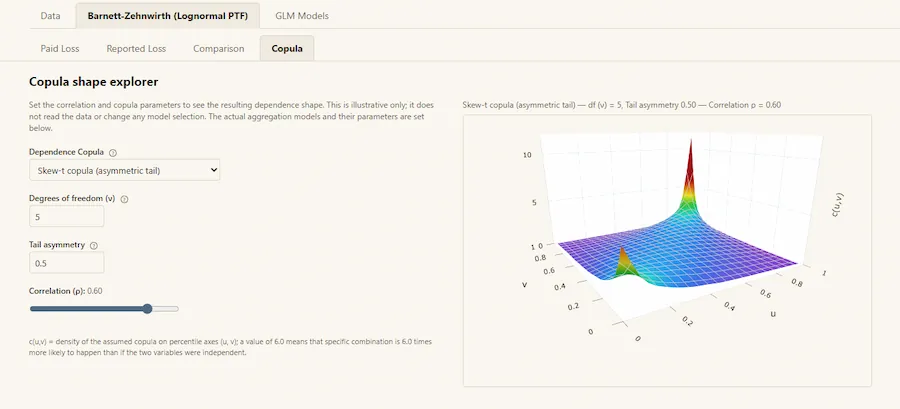

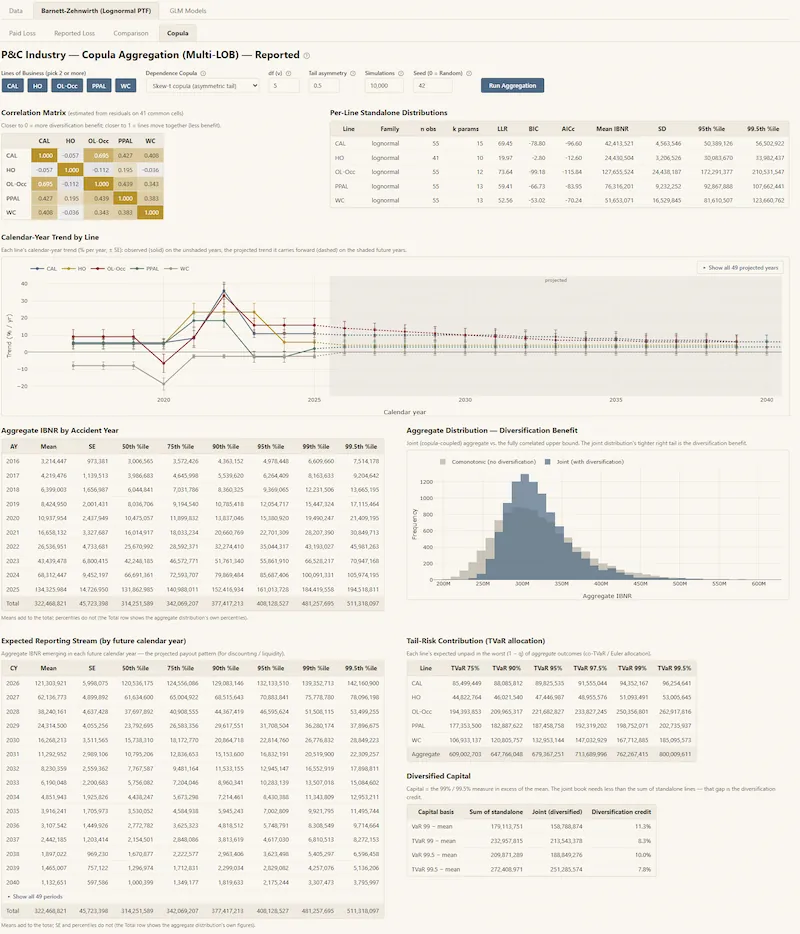

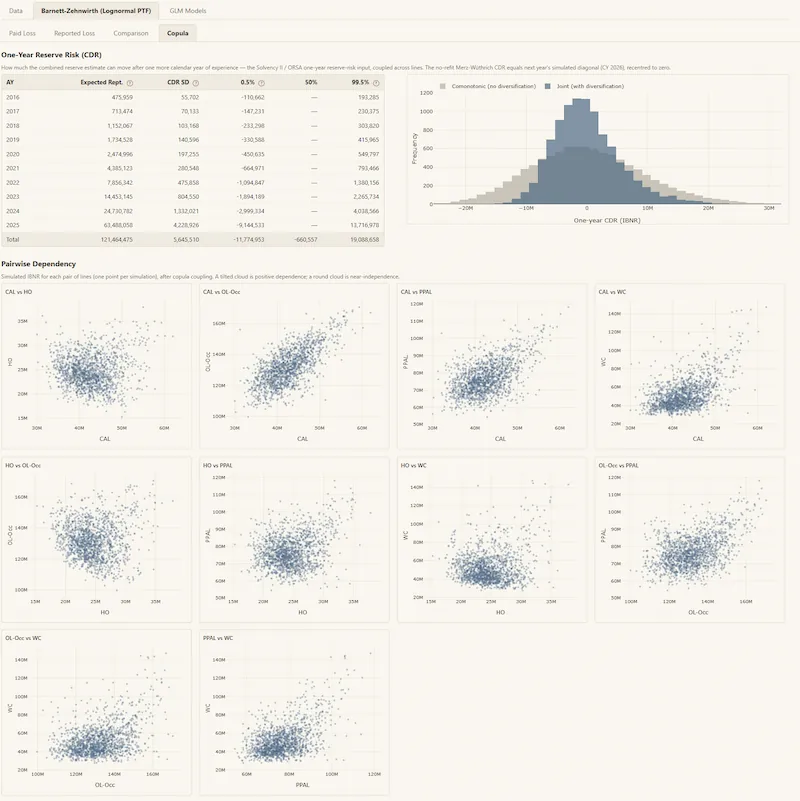

BASR aggregates results across multiple lines of business or segments into an overall loss distribution by measuring correlations from the data and reflecting tail dependencies through customizable copula forms (including a visualizer to assist in modeling decisions).

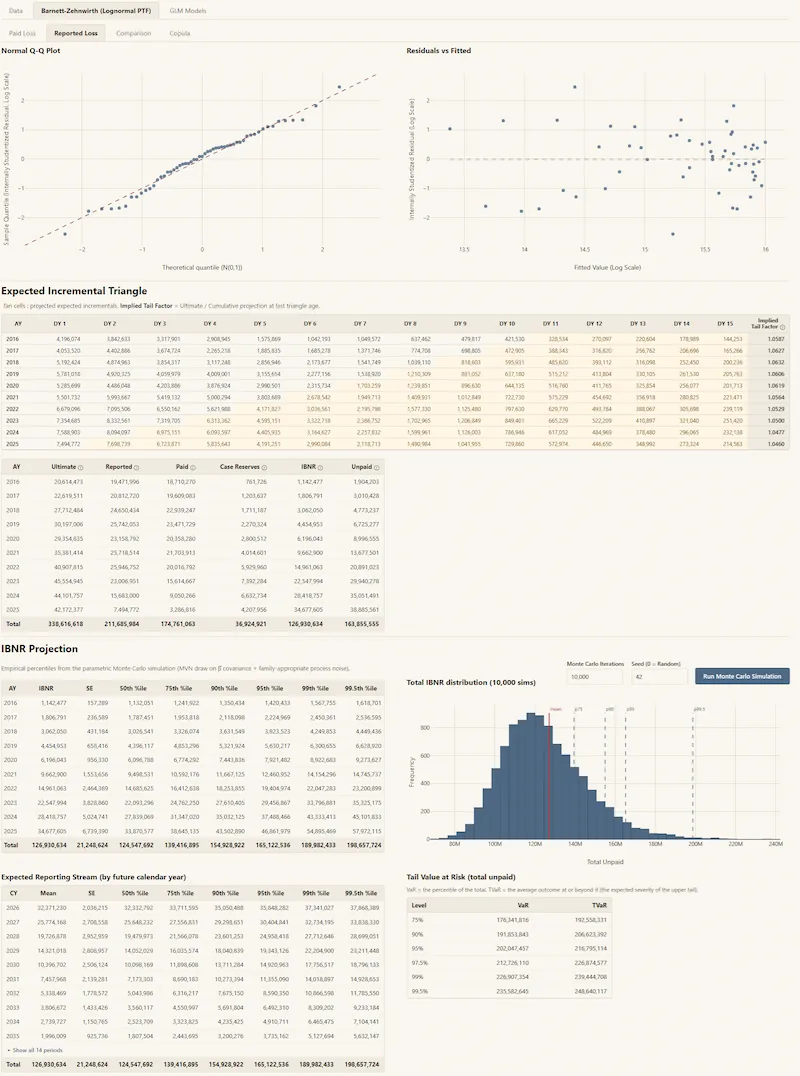

BASR produces the full predictive distribution of unpaid claims, by accident period and in total, with percentiles, reserve ranges, a one-year claims development result (CDR), and insights into historical trends, valuable not only to the reserving process but also to ratemaking, risk management, and capital modeling.

BASR is now live for advisory engagements and will be available for commercial licensing soon. Schedule a meeting or send an email to inquire about either.